For many Americans in 2026, credit card interest rates have become an insurmountable wall. If your score isn't high enough for a consolidation loan or a 0% balance transfer card, a Debt Management Plan (DMP) is often the most effective "middle ground" between struggling alone and filing for bankruptcy.

A DMP is not a loan. It is a structured repayment program managed by a non-profit credit counseling agency that negotiates directly with your creditors to lower your interest rates and eliminate fees.

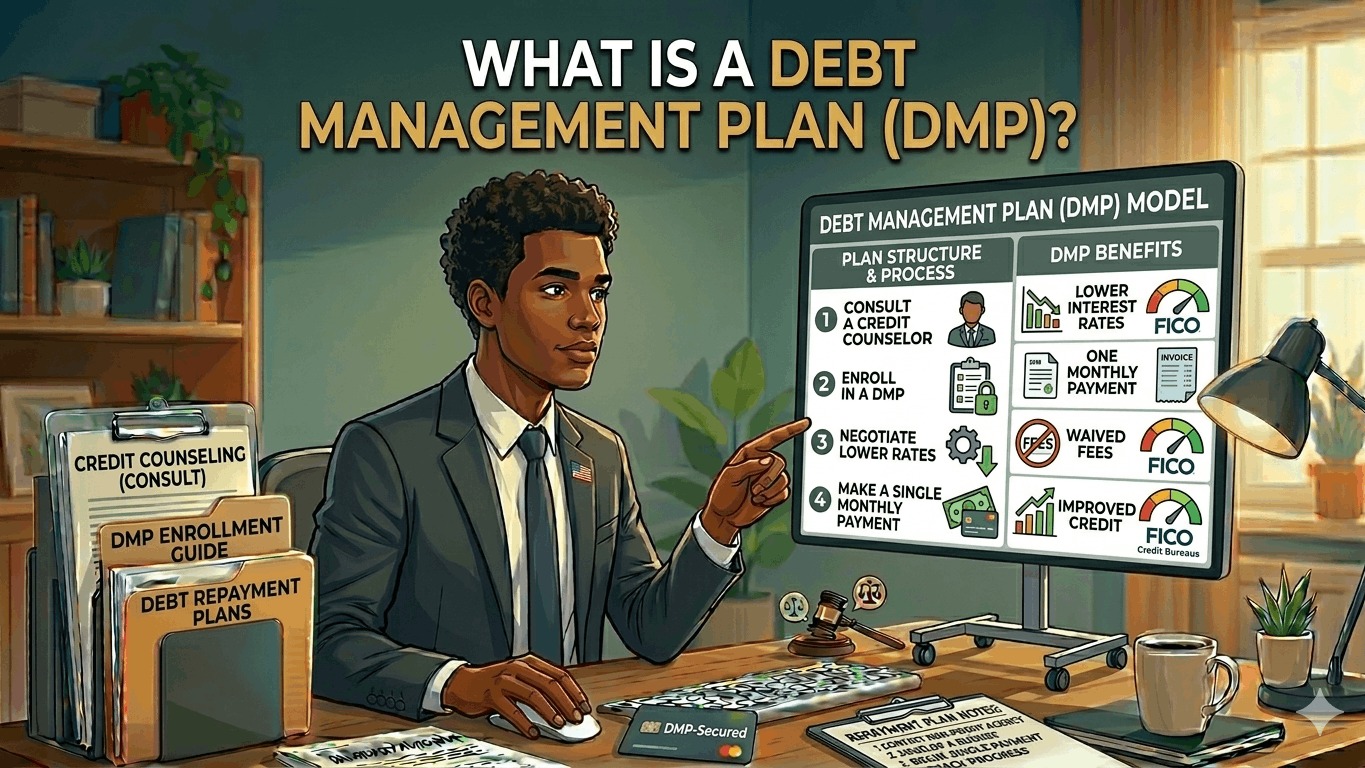

1. How a DMP Works in 2026

Unlike debt settlement (where you stop paying) or consolidation (where you borrow new money), a DMP focuses on repaying your full principal under much better terms.

- The Negotiation: A certified credit counselor contacts your card issuers (Chase, Amex, etc.). Because the counselor represents a non-profit, banks are often willing to drop interest rates from 24% down to 8% or even 0%.

- The Single Payment: You make one monthly payment to the credit counseling agency. They then distribute that money to each of your creditors on your behalf.

- The 3-to-5 Year Timeline: DMPs are designed with a clear "finish line." Most plans are structured to have you 100% debt-free within 36 to 60 months.

2. Who is the Ideal Candidate?

In the current 2026 economy, DMPs are specifically designed for people who:

- Have Unsecured Debt: This includes credit cards, medical bills, and some personal loans. It does not cover "secured" debt like car loans or mortgages.

- Can’t Get a Loan: If your credit score is below 660, you likely won't qualify for a low-interest consolidation loan. DMPs do not require a credit check to join.

- Have Steady Income: You must have enough monthly income to cover the negotiated payment.

3. The Impact on Your Credit Score

There is a common myth that a DMP ruins your credit. Here is the 2026 reality:

- No "Hard Pull": Enrolling in a DMP does not require a hard credit inquiry.

- The "Closed Account" Dip: You are required to close the credit cards included in the plan. This can cause a temporary dip in your score because it reduces your “Total Available Credit.”

- The Long-Term Spike: As you make consistent, on-time payments through the agency, your "Payment History" (35% of your score) strengthens. Most people see their scores increase significantly by the second year of the plan.

4. The Pros and Cons of a DMP

Pros:

- Interest Savings: Cutting your APR in half (or more) saves you thousands of dollars over 5 years.

- Stops the Calls: Once you are on a DMP, creditors generally stop collection calls and late fee charges.

- No New Debt: Because the accounts are closed, you are forced to live on a cash/debit budget, breaking the cycle of overspending.

Cons:

- Account Closure: You cannot use the cards in the plan. Most agencies allow you to keep one card out of the plan for emergencies, but even that is up to the creditor's discretion.

- Fees: While the counseling is often free, the plan itself usually has a small monthly maintenance fee (average $30–$50) to cover the agency's administration costs.

- Commitment: If you miss a payment to the agency, your creditors can kick you out of the plan and instantly revert your interest rates to the original 24%+.

5. How to Start a DMP in the USA

To ensure you are working with a legitimate agency, only use organizations accredited by the National Foundation for Credit Counseling (NFCC) or the Financial Counseling Association of America (FCAA).

- Initial Counseling: You’ll spend 45–60 minutes on a call (or video chat) reviewing your budget and debt.

- The Proposal: The counselor will show you exactly what your new monthly payment and interest rates would be.

- Acceptance: Once you agree, the agency sends the proposal to your banks. Payments usually begin within 30 days.