In the housing market, mortgage insurance remains a vital—yet often misunderstood—tool that allows buyers to purchase a home without a 20% down payment. While it adds an extra cost to your monthly budget, it is the "key" that unlocks homeownership for millions of Americans.

Understanding the difference between the types of insurance and knowing the exact moment you can stop paying it can save you thousands of dollars over the life of your loan.

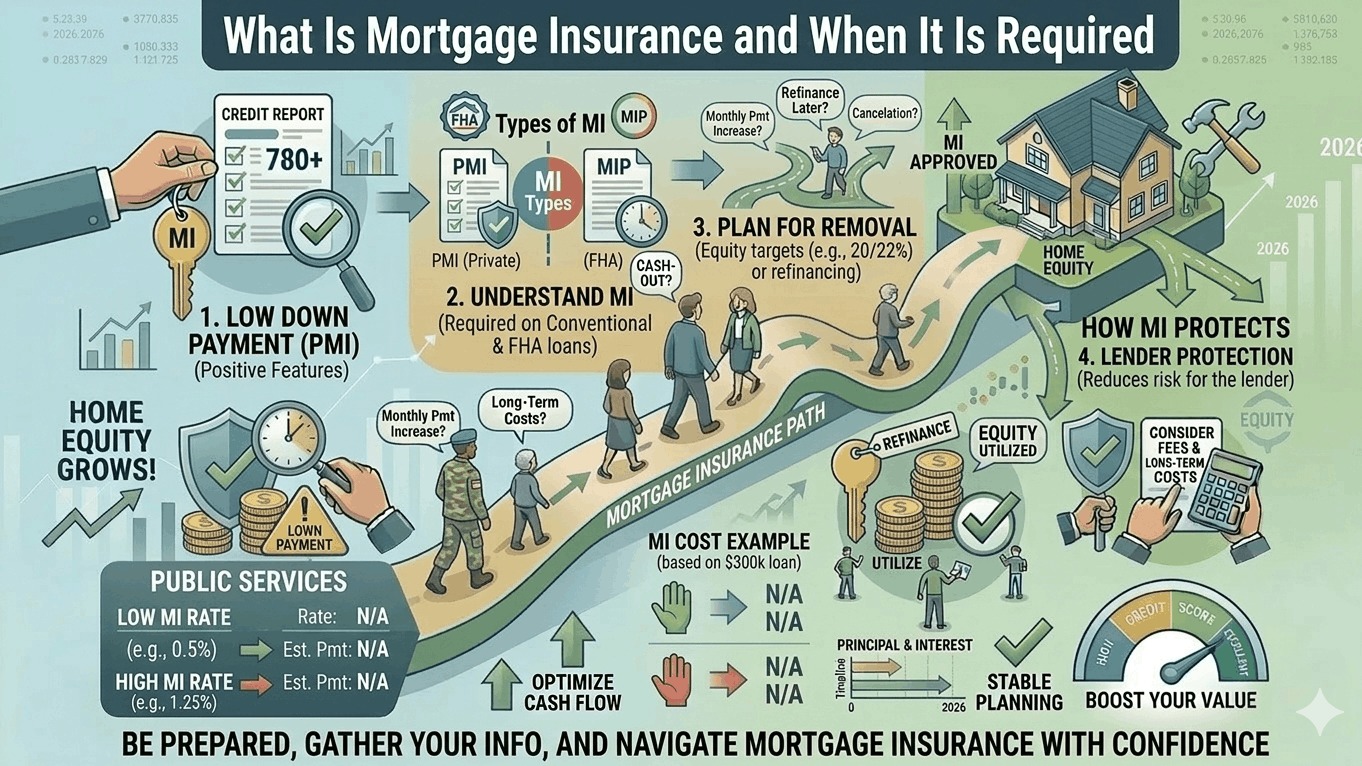

1. What Exactly Is Mortgage Insurance?

Mortgage insurance is a policy that protects the lender, not the borrower. If you fall behind on your payments and the home goes into foreclosure, this insurance compensates the lender for a portion of their loss.

It is generally required when a borrower’s Loan-to-Value (LTV) ratio is higher than 80% (meaning your down payment was less than 20%).

2. The Two Main Types of Mortgage Insurance

A. Private Mortgage Insurance (PMI)

PMI is used for Conventional loans. It is provided by private companies and is usually paid as a monthly premium added to your mortgage payment.

- Cost: In 2026, PMI typically costs between 0.46% and 1.5% of the total loan amount per year.

- The "Exit" Strategy: PMI is removable. Once you reach 20% equity in your home, you can request to have it cancelled. By law, the lender must automatically cancel it once you reach 22% equity.

B. Mortgage Insurance Premium (MIP)

MIP is required for all FHA loans, regardless of the down payment amount.

- The Structure: You pay both an Upfront MIP (usually 1.75% of the loan, often rolled into the balance) and an Annual MIP (paid monthly).

- The "Lifetime" Rule: If you put down less than 10% on an FHA loan, you must pay MIP for the entire life of the loan. The only way to remove it is to refinance into a Conventional loan once you have enough equity.

3. When Is Mortgage Insurance Required?

Lenders in 2026 strictly mandate insurance in the following scenarios:

| Loan Type | Down Payment | Insurance Requirement |

|---|---|---|

| Conventional | < 20% | PMI Required until 20% equity. |

| FHA | Any Amount | MIP Required (usually for the life of the loan). |

| USDA | 0% | Guarantee Fee (Upfront + Monthly) is required. |

| VA | 0% | None. VA loans do not have monthly mortgage insurance. |

4. How Much Will It Cost You?

In 2026, your specific mortgage insurance rate is determined by three factors:

- Credit Score: Higher scores (760+) receive significantly lower PMI rates.

- Down Payment: A 15% down payment results in much cheaper insurance than a 3% down payment.

- Loan Type: FHA rates are standardized, while Conventional PMI rates vary by the insurance provider.

Example: On a $400,000 home with 3% down, a borrower with a 740 credit score might pay $160 per month in PMI.