One of the biggest myths in American real estate is that you need a 20% down payment to buy a home. While 20% remains the benchmark for avoiding certain costs, the reality in 2026 is far more flexible. With the average U.S. home price sitting near $420,000, waiting to save $84,000 is simply not feasible for many first-time buyers.

This guide breaks down the actual minimums required for various loan types and the pros and cons of putting more (or less) money down.

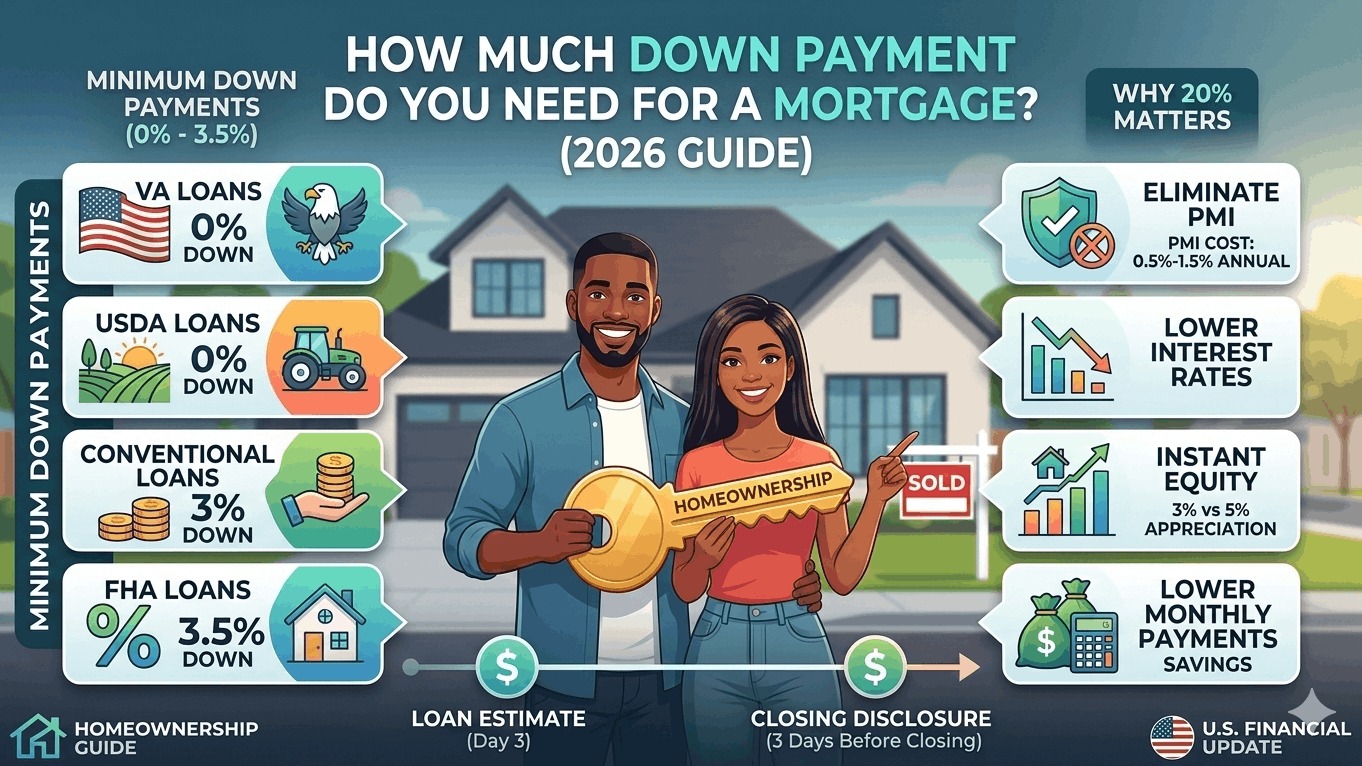

1. Minimum Down Payment Requirements by Loan Type

The amount you need depends largely on the type of mortgage you choose. In 2026, these are the standard minimums:

- Conventional Loans: As little as 3% down. These are the most common loans for borrowers with strong credit (720+).

- FHA Loans: 3.5% down. Insured by the Federal Housing Administration, these are designed for borrowers with lower credit scores (down to 580).

- VA Loans: 0% down. Available to veterans, active-duty service members, and eligible surviving spouses.

- USDA Loans: 0% down. Available for homes in designated rural and some suburban areas for low-to-moderate-income borrowers.

- Jumbo Loans: Usually 10% to 20% down. These are for luxury homes that exceed local conforming loan limits.

2. The 20% Rule: Why It Still Matters

While you can buy with 3%, there are significant financial benefits to hitting the 20% mark:

- Eliminate PMI: If you put down less than 20%, lenders require Private Mortgage Insurance (PMI). This typically costs between 0.5% and 1.5% of your loan amount annually, added to your monthly payment.

- Lower Interest Rates: Lenders offer their "prime" rates to those with more equity. A 20% down payment could lower your rate by 0.25% to 0.50% compared to a 3% down payment.

- Instant Equity: You start your homeownership journey owning one-fifth of the asset, providing a buffer if home prices fluctuate.

- Lower Monthly Payments: A larger down payment means a smaller loan, which results in less interest paid over 30 years.

3. The Cost of Waiting vs. Buying Now

In a market where home values are appreciating at 3% to 5% per year, waiting to save a full 20% can actually cost you more in the long run.

Example: You want a $400,000 home.

- If you buy now with 3.5% down ($14,000), you start building equity immediately.

- If you wait three years to save 20% ($80,000), that same home might now cost $440,000, meaning your 20% goal just climbed to $88,000.

[Image: Infographic comparing monthly payments of 3% vs 20% down]

4. Where to Find Down Payment Funds

If you don't have the cash sitting in a savings account, consider these 2026-compliant sources:

- Gifts: Most loan programs allow family members to "gift" you the down payment, provided there is a signed letter stating it is not a loan.

- 401(k) Loans: Many employers allow you to borrow against your retirement for a primary residence purchase without the 10% early withdrawal penalty.

- DPA Programs: There are over 2,000 Down Payment Assistance (DPA) programs across the USA. Many offer forgivable grants or low-interest second mortgages to cover your 3.5% requirement.