If you are juggling multiple credit card payments, medical bills, or personal loans, you’ve likely heard the term debt consolidation. In 2026, with average credit card interest rates hovering near 23%, consolidation has become a vital survival tool for Americans looking to escape high-interest traps.

Debt consolidation is essentially a "reset" for your debt structure. It doesn't make the debt disappear, but it changes how you pay it back.

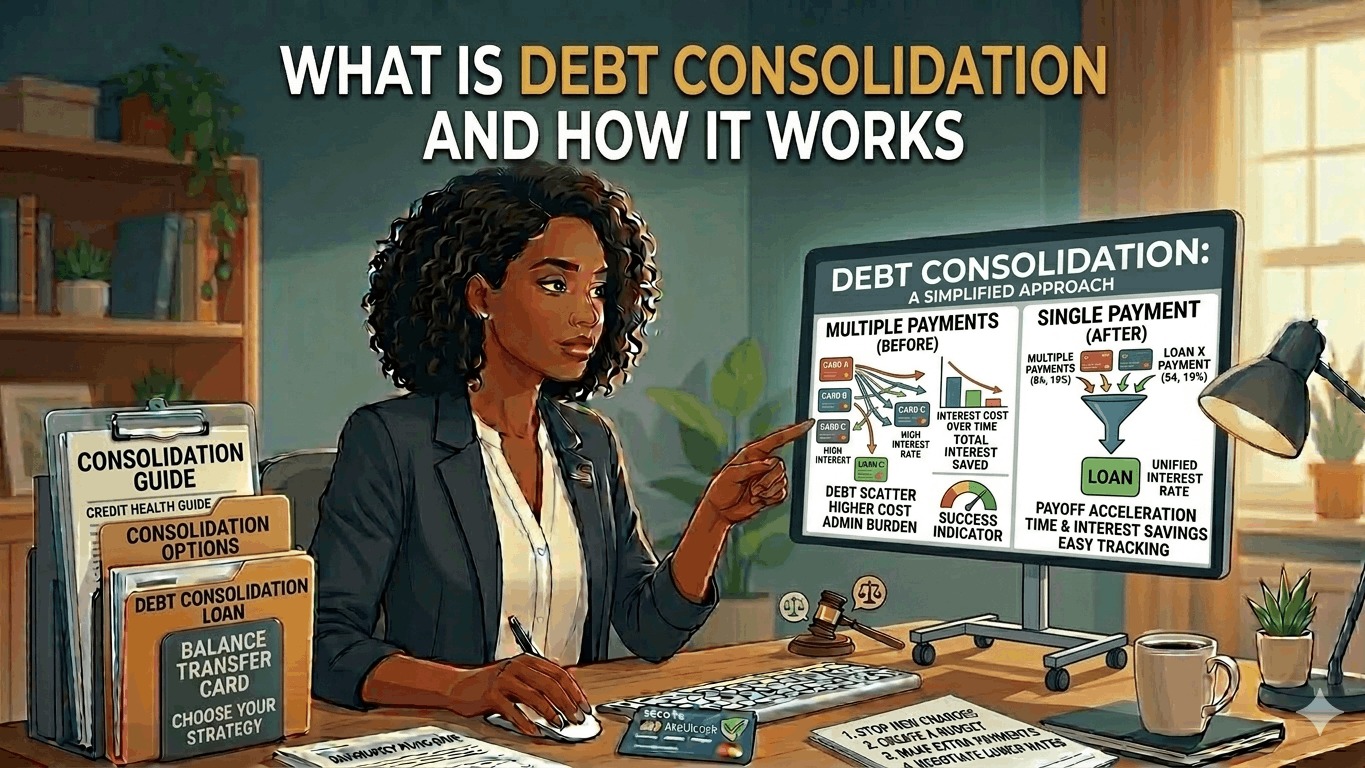

1. The Simple Definition

Debt consolidation is the process of taking out a new loan to pay off multiple existing debts. Instead of sending five checks to five different lenders every month, you use one big loan to wipe those balances to $0. Now, you only have one monthly payment to one lender.

The Two Main Goals:

- Lower Interest: Swapping a 25% APR credit card for a 10% APR personal loan saves you thousands in interest.

- Simplicity: One due date reduces the risk of missing a payment and incurring late fees.

2. How the Process Works (Step-by-Step)

In 2026, the consolidation process is faster than ever, often handled entirely through mobile apps with same-day funding.

- Inventory Your Debt: Total up every balance you want to clear. Note the interest rate for each to ensure your new loan is actually a better deal.

- Apply for a Consolidation Tool: This is usually a Personal Loan or a Balance Transfer Credit Card.

- Pay Off Your Creditors: Once approved, the new lender may pay your old creditors directly, or they will deposit the cash into your bank account for you to pay them yourself.

- Close the Loop: Your old cards now show a $0 balance. You then begin making fixed monthly payments on your new, lower-interest consolidation loan.

3. Popular Consolidation Methods in 2026

Depending on your credit score and financial situation, you have three primary paths:

A. Personal Debt Consolidation Loans

These are unsecured loans with fixed interest rates.

- Pros: Fixed monthly payments and a clear "end date" (usually 2–5 years).

- Best for: Borrowers with a "Good" credit score (670+) who want a structured payoff plan.

B. 0% APR Balance Transfer Cards

You move your debt to a new credit card that charges 0% interest for an introductory period (up to 21 months in 2026).

- Pros: You pay zero interest during the intro period.

- Cons: You must pay a transfer fee (3–5%) and pay off the full balance before the 0% window slams shut.

C. Home Equity (HELOC or Home Equity Loans)

Homeowners can borrow against their house to pay off high-interest unsecured debt.

- Pros: The lowest interest rates available.

- Cons: Extreme Risk. You are turning unsecured credit card debt into secured debt. If you can't make the payments, the bank can foreclose on your home.

4. The "Hidden" Impact on Your Credit Score

Consolidation usually follows a specific credit score trajectory:

- The Initial Dip: Applying for a new loan triggers a "hard inquiry," which may drop your score by a few points.

- The Massive Spike: When you use the loan to pay off your credit cards, your Credit Utilization Ratio (how much of your limit you're using) drops to near 0%. This is the second biggest factor in your score and can cause a jump of 50+ points within a month.

5. Is Consolidation Right for You?

Consolidation is a mathematical tool, but debt is often a behavioral issue.

- It works if: You have a steady income, a better interest rate, and the discipline to stop using the credit cards once they are at $0.

- It fails if: You see the $0 balance on your cards as "room to spend" and run the balances back up while still owing the consolidation loan. This is known as "Double Debt" and is the #1 pitfall of consolidation.