When you're shopping for a loan, one of the first terms you'll encounter is secured or unsecured. While both allow you to borrow money, they work differently and can have a significant impact on your interest rate, approval chances, borrowing limits, and financial risk.

Understanding the difference between secured and unsecured loans can help you choose the right option for your situation. In many cases, the better choice isn't simply the one with the lowest interest rate—it's the one that fits your financial goals and comfort level.

This guide explains secured and unsecured loans in simple terms, compares their advantages and disadvantages, and provides practical examples to help you make an informed borrowing decision.

What Is a Secured Loan?

A secured loan is backed by collateral—an asset that the lender can claim if you fail to repay the loan.

Common types of collateral include:

- A home

- A vehicle

- A savings account

- Investments

- Other valuable property

Because collateral reduces the lender's risk, secured loans often come with lower interest rates and higher borrowing limits.

What Is an Unsecured Loan?

An unsecured loan does not require collateral. Instead, the lender decides whether to approve your application based on factors such as your credit history, income, employment, and existing debt.

If you fail to repay an unsecured loan, the lender cannot automatically take your property. However, they may report missed payments to credit bureaus, charge late fees, send the account to collections, or pursue legal action depending on the circumstances.

Most personal loans and many credit cards fall into this category.

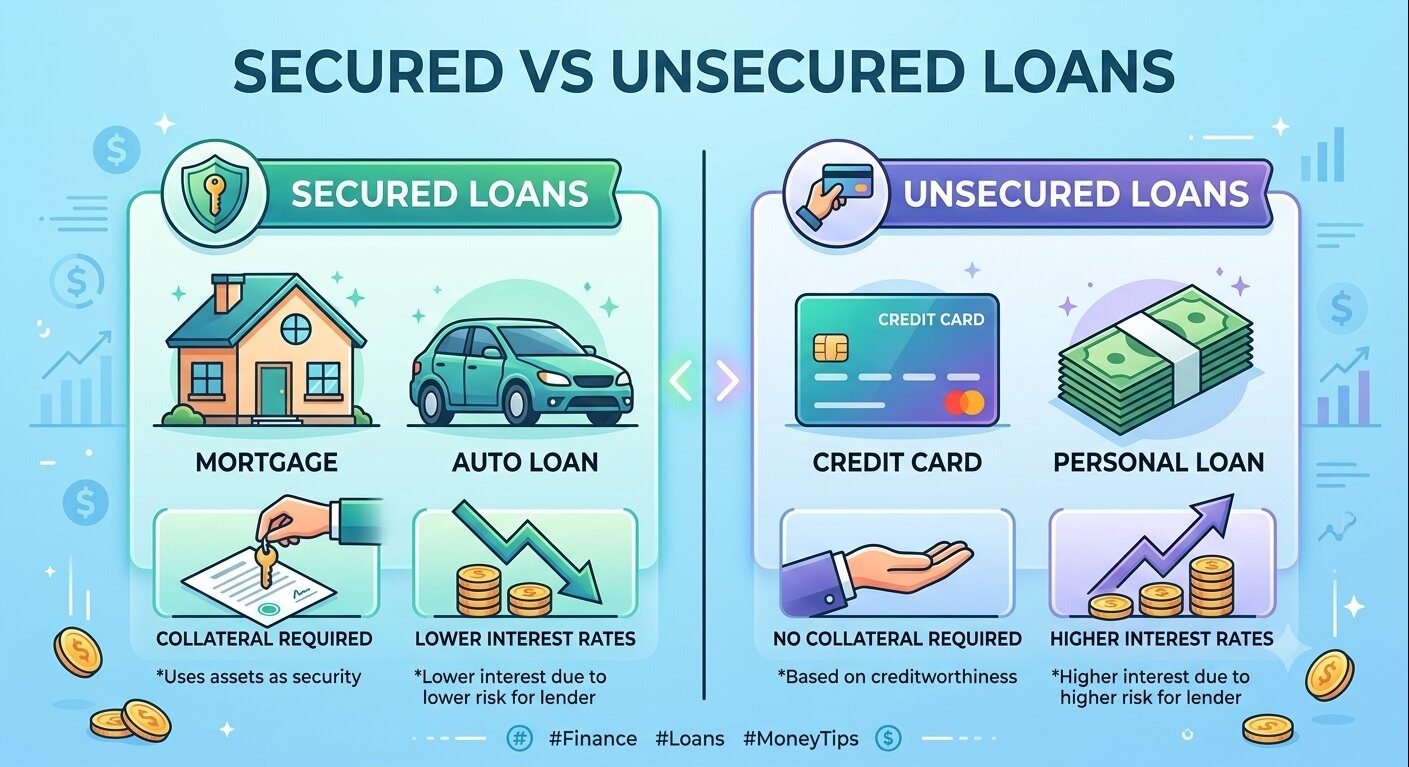

Secured vs Unsecured Loans at a Glance

| Feature | Secured Loan | Unsecured Loan |

|---|---|---|

| Collateral Required | Yes | No |

| Interest Rate | Usually lower | Usually higher |

| Approval Requirements | Often easier | Usually stricter |

| Loan Amount | Higher borrowing limits | Moderate borrowing limits |

| Risk to Borrower | Could lose collateral | No collateral at risk |

| Best For | Large purchases | Everyday borrowing and smaller expenses |

Common Examples of Secured Loans

Several familiar loan products are secured by assets.

These include:

- Mortgage loans

- Auto loans

- Home equity loans

- Home equity lines of credit (HELOCs)

- Secured personal loans

- Secured business loans

Because lenders have collateral, these loans generally offer competitive interest rates.

If you're exploring different borrowing options, start with Types of Loans in the USA Explained:

https://statush.com/credit-score-debt/types-of-loans-in-the-usa-explained

Common Examples of Unsecured Loans

Unsecured loans are popular because borrowers don't have to risk valuable assets.

Examples include:

- Personal loans

- Student loans (many federal loans)

- Credit cards

- Medical financing

- Some online installment loans

Approval usually depends on your financial profile rather than property ownership.

Learn more in How Personal Loans Work:

https://statush.com/credit-score-debt/how-personal-loans-work

Real-World Example

Imagine two friends need to borrow $20,000.

Emily owns a home with significant equity. She qualifies for a secured home equity loan at a relatively low interest rate because her home acts as collateral.

Jason rents an apartment and applies for an unsecured personal loan. Since he doesn't offer collateral, the lender evaluates his income and credit score before approving the loan. His interest rate is higher, but he doesn't risk losing property if financial difficulties arise.

Both loans provide the money they need, but the costs and risks are very different.

Advantages of Secured Loans

Secured loans offer several benefits.

Lower Interest Rates

Since the lender has collateral, they typically charge lower interest rates than unsecured loans.

Higher Loan Amounts

Borrowers may qualify for larger loan amounts because the lender has additional protection.

Easier Approval

Applicants with average or limited credit histories may have an easier time qualifying if they can provide valuable collateral.

Longer Repayment Terms

Many secured loans allow repayment over longer periods, helping reduce monthly payments.

Disadvantages of Secured Loans

Secured borrowing isn't without risks.

You Could Lose Your Asset

If you stop making payments, the lender may repossess the collateral.

For example:

- Missing mortgage payments could lead to foreclosure.

- Missing auto loan payments could result in vehicle repossession.

Longer Approval Process

The lender may need to evaluate the collateral before approving the loan, making the process slower than some unsecured loans.

Advantages of Unsecured Loans

Many borrowers prefer unsecured loans for their flexibility.

No Collateral Needed

You don't need to own valuable assets to qualify.

Faster Approval

Many online lenders approve unsecured personal loans within a day or two.

Lower Personal Risk

Although missed payments hurt your credit, your house or vehicle isn't automatically at risk.

Disadvantages of Unsecured Loans

There are trade-offs.

- Higher interest rates

- Smaller borrowing limits

- Stronger credit requirements

- Higher monthly payments for some borrowers

Applicants with poor credit may receive less favorable loan offers or face difficulty qualifying.

If your credit isn't perfect, read Best Loan Options for Bad Credit:

https://statush.com/credit-score-debt/best-loan-options-for-bad-credit

Which Loan Costs Less?

In most situations, secured loans cost less because lenders face lower financial risk.

However, a lower interest rate doesn't automatically make a secured loan the better choice.

For example, borrowing against your home to pay for a vacation usually isn't a wise financial decision. The potential savings in interest aren't worth putting your home at risk for a discretionary expense.

Always compare:

- Interest rate

- Total borrowing cost

- Monthly payment

- Fees

- Risk of losing collateral

How Lenders Decide Which Loan You Qualify For

Whether you're applying for a secured or unsecured loan, lenders typically evaluate:

- Credit score

- Credit history

- Income

- Employment stability

- Debt-to-income ratio

- Existing financial obligations

For secured loans, they'll also assess the value of the collateral.

Learn more in:

- Loan Approval Factors Explained

https://statush.com/credit-score-debt/loan-approval-factors-explained - How Debt-to-Income Ratio Affects Loans

https://statush.com/credit-score-debt/how-debt-to-income-ratio-affects-loans

Practical Tips Before Choosing

Before deciding between secured and unsecured borrowing, keep these tips in mind.

- Only pledge collateral if you're confident you can repay the loan.

- Compare offers from several lenders.

- Don't focus solely on the monthly payment—consider the total interest you'll pay.

- Read all loan terms, including fees and penalties.

- Borrow only what you genuinely need.

Taking a little extra time to compare options can save money and reduce financial stress later.

Common Mistakes to Avoid

Borrowers often make avoidable mistakes when choosing between loan types.

Some of the most common include:

- Using home equity for unnecessary spending

- Accepting the first loan offer without comparing lenders

- Ignoring origination fees and closing costs

- Borrowing more than needed

- Missing payments and damaging credit

- Assuming every secured loan is automatically the cheapest option

Making informed decisions starts with understanding both the benefits and the risks.

Final Thoughts

Secured and unsecured loans each serve an important purpose. Secured loans generally offer lower interest rates and larger borrowing limits but require collateral that could be at risk if payments are missed. Unsecured loans provide greater flexibility and don't require valuable assets, though they often come with higher interest rates and stricter approval requirements.

The best choice depends on your financial situation, borrowing purpose, and ability to comfortably repay the loan. By comparing multiple lenders, understanding the total borrowing cost, and selecting the right loan type, you can borrow with greater confidence and avoid unnecessary financial pitfalls.

To continue learning, explore How Interest Works on Loans, Fixed vs Variable Interest Rates, and How to Qualify for a Personal Loan to better understand how borrowing costs are calculated and how to improve your chances of getting the best loan terms.

Related Articles

- How Interest Works on Loans

https://statush.com/credit-score-debt/how-interest-works-on-loans - Fixed vs Variable Interest Rates

https://statush.com/credit-score-debt/fixed-vs-variable-interest-rates - How to Qualify for a Personal Loan

https://statush.com/credit-score-debt/how-to-qualify-for-a-personal-loan