Taking out your first personal loan can feel overwhelming. With so many lenders advertising low interest rates, fast approvals, and flexible repayment terms, it's easy to wonder which loan is actually the best choice.

The truth is that there isn't one "best" personal loan for everyone. The right loan depends on your financial situation, credit history, borrowing needs, and ability to repay. As a beginner, your goal shouldn't simply be getting approved—it should be finding a loan that's affordable, transparent, and easy to manage.

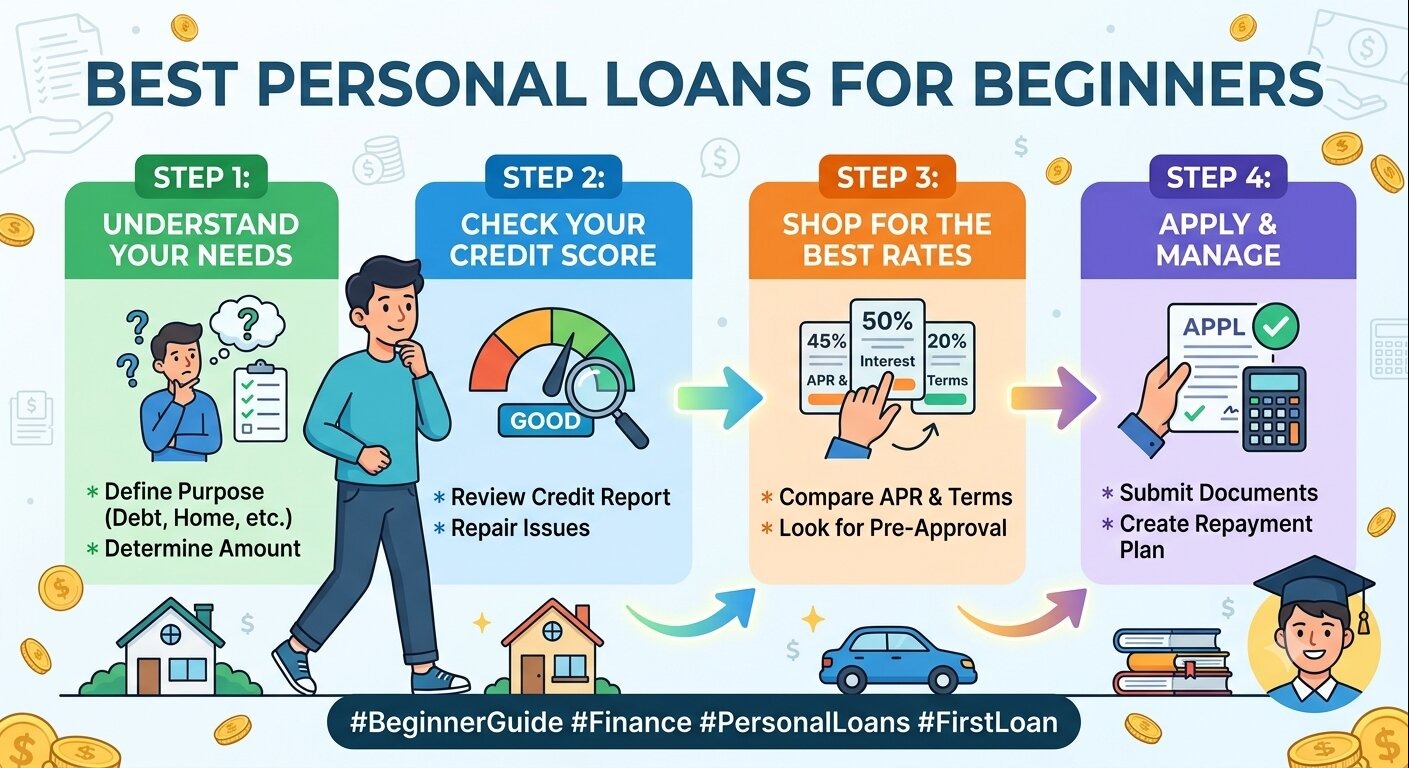

This guide explains what beginners should look for in a personal loan, how lenders evaluate applications, and practical tips for choosing the right borrowing option.

What Is a Personal Loan?

A personal loan is an installment loan that provides a lump sum of money. You repay the loan through fixed monthly payments over a set period, usually between two and seven years.

Unlike auto loans or mortgages, personal loans can typically be used for almost any legitimate purpose.

Common reasons people borrow include:

- Emergency expenses

- Medical bills

- Home improvements

- Debt consolidation

- Wedding expenses

- Moving costs

- Large purchases

If you're new to borrowing, start by reading How Personal Loans Work:

https://statush.com/credit-score-debt/how-personal-loans-work

What Beginners Should Look For

Instead of choosing the lender with the biggest advertisement, compare the features that actually affect your borrowing costs.

| Feature | Why It Matters |

|---|---|

| Interest Rate | Lower rates reduce total borrowing costs. |

| Monthly Payment | Should comfortably fit your budget. |

| Loan Term | Longer terms lower monthly payments but increase total interest. |

| Fees | Watch for origination fees, late fees, and other charges. |

| Customer Reviews | Good service can make repayment easier. |

| Prepayment Option | Allows you to pay off the loan early without penalties. |

Comparing several lenders before applying often leads to better loan offers.

Who Can Apply?

Most lenders require applicants to meet basic eligibility requirements.

These commonly include:

- Being at least 18 years old

- Having a steady source of income

- Providing identification

- Having a checking account

- Meeting minimum credit requirements

Some online lenders also consider applicants with limited credit histories, making them attractive options for first-time borrowers.

Real-World Example

Imagine Alex recently graduated from college and needs $8,000 to cover moving expenses and purchase furniture for a new apartment.

Instead of using several high-interest credit cards, Alex compares personal loan offers from multiple lenders. After reviewing interest rates, fees, and repayment terms, Alex chooses a loan with fixed monthly payments that comfortably fits the monthly budget.

Because the payments are predictable, it's easier to plan expenses while gradually building a positive credit history.

Understanding Interest Rates

Interest is the cost of borrowing money.

Generally, borrowers with:

- Higher credit scores

- Stable income

- Lower existing debt

receive lower interest rates.

Even a small difference in interest rates can save hundreds of dollars during the life of the loan.

For a detailed explanation, read How Interest Works on Loans:

https://statush.com/credit-score-debt/how-interest-works-on-loans

Fixed vs Variable Rates

Many beginner-friendly personal loans offer fixed interest rates.

This means:

- Monthly payments stay the same.

- Budgeting becomes easier.

- Interest costs remain predictable.

Variable-rate loans may begin with lower rates, but payments can increase if interest rates rise.

Learn more in Fixed vs Variable Interest Rates:

https://statush.com/credit-score-debt/fixed-vs-variable-interest-rates

How Much Should You Borrow?

One of the biggest mistakes first-time borrowers make is accepting the maximum amount they're approved for.

Instead, borrow only what you actually need.

For example:

If you need $7,500 for home repairs, borrowing $12,000 simply because you're approved means paying interest on an extra $4,500 that wasn't necessary.

Smaller loans are generally easier to repay and reduce overall borrowing costs.

Comparing Loan Offers

Before accepting any loan, compare multiple lenders.

Look beyond the advertised interest rate and consider:

- Annual Percentage Rate (APR)

- Loan term

- Monthly payment

- Total repayment cost

- Fees

- Early repayment options

- Customer support

The lowest monthly payment isn't always the cheapest loan. A longer repayment period may reduce monthly payments while significantly increasing the total interest paid.

Common Fees to Watch For

Some lenders charge additional fees that increase the total cost of borrowing.

These may include:

- Origination fees

- Late payment fees

- Returned payment fees

- Prepayment penalties (less common today)

Always read the loan agreement before signing.

Learn more in Loan Origination Fees Explained:

https://statush.com/credit-score-debt/loan-origination-fees-explained

Improving Your Approval Chances

If you're applying for your first personal loan, a few simple steps can improve your chances of approval.

- Check your credit report for errors.

- Pay existing bills on time.

- Reduce outstanding credit card balances.

- Avoid applying for several loans at once.

- Keep your debt-to-income ratio as low as possible.

- Provide accurate financial information.

Lenders appreciate applicants who demonstrate stable finances and responsible borrowing habits.

For more information, read:

- How to Qualify for a Personal Loan

https://statush.com/credit-score-debt/how-to-qualify-for-a-personal-loan - Loan Approval Factors Explained

https://statush.com/credit-score-debt/loan-approval-factors-explained

Practical Tips for First-Time Borrowers

If this is your first loan, keep these practical tips in mind:

- Create a repayment budget before borrowing.

- Set up automatic payments to avoid missing due dates.

- Borrow only for important financial needs.

- Compare offers from banks, credit unions, and online lenders.

- Keep copies of your loan agreement and payment schedule.

- Pay more than the minimum payment whenever possible.

Responsible borrowing today can make it easier to qualify for better loan terms in the future.

Common Mistakes to Avoid

Many beginners make avoidable borrowing mistakes.

Try not to:

- Focus only on monthly payments.

- Ignore the total interest you'll pay.

- Borrow more than necessary.

- Skip reading the loan agreement.

- Miss payment deadlines.

- Apply with multiple lenders without researching your options.

Making informed decisions now can save money and protect your credit score over the long term.

Is a Personal Loan Right for Beginners?

A personal loan can be an excellent financial tool when used responsibly. If you have a clear purpose for borrowing, understand the repayment terms, and choose a loan that fits your budget, it can provide convenient access to funds while helping you establish a positive credit history.

However, borrowing should never become a substitute for regular budgeting or emergency savings. Always consider whether the loan is necessary and whether you can comfortably make the monthly payments.

Final Thoughts

For beginners, the best personal loan isn't necessarily the one with the largest loan amount or the fastest approval. It's the one that offers affordable payments, reasonable interest rates, transparent fees, and terms that fit your financial situation.

Take time to compare lenders, understand the total cost of borrowing, and avoid borrowing more than you need. A thoughtful approach to your first personal loan can help you build financial confidence while avoiding unnecessary debt.

As you continue learning about borrowing, explore the articles below to deepen your understanding of loan costs, repayment strategies, and qualification requirements.

Related Articles

- Types of Loans in the USA Explained

https://statush.com/credit-score-debt/types-of-loans-in-the-usa-explained - How to Qualify for a Personal Loan

https://statush.com/credit-score-debt/how-to-qualify-for-a-personal-loan - How Interest Works on Loans

https://statush.com/credit-score-debt/how-interest-works-on-loans - How to Calculate Loan Payments

https://statush.com/credit-score-debt/how-to-calculate-loan-payments - Best Strategies to Reduce Loan Interest

https://statush.com/credit-score-debt/best-strategies-to-reduce-loan-interest